France decided, Emmanuel Macron is now the President of France. I will not shout some ‘hack’ issue. I believe that France made a choice, how well the choice is, is something that the President-elect of France will have to prove to be. Not the lame statistics on how young he is. The Guardian gives us some of the optional bad news (at https://www.theguardian.com/world/2017/may/07/theresa-may-congratulates-macron-on-victory-as-eu-breathes-sigh-of-relief) where we see: “Happy that the French have chosen a European future. Together for a stronger and fairer Europe.” No, they did not and your rhetoric only is a first piece of evidence that the EU and the ECB are considering a former investment banker to be the reason to play your games, forcing people deeper in debt and slowly turning the EU into something despicable. For the most, the article is fine. Today will be all about congratulating President Macron, whilst those shaking hands, calling the Palace or sending letters are desperately trying to get a few political punches in. That is part of the game, yet the dangers due to the greedy need of the USA is about to become actually dangerous. Marine Le Pen could have sunk those dangers, although it would come with other issues, there is no denying that. Yet the economic health is going to be a first, in that Crédit Agricole, BNP Paribas and Natixis would guard against that happening to France (after they take care of themselves and their needs), yet will it be enough? The quote that President Macron is giving now is: “I do consider that my mandate, the day after, will be at the same time to reform in depth the European Union and our European project,” Macron had told reporters, adding that if he were to allow the EU to continue to function as it was would be a “betrayal”. It sounds nice, but over time and especially as we watch delay after delay will we see if he is actually made of stern stuff. Time will tell and there is no way that it would be regarded as fair to see any initial headway until at least 10 days post forming his government. Yet there is a side we must take heed from. It is seen in the quote “he spoke out against a “tailormade approach where the British have the best of two worlds” creating “an incentive for others to leave and kill the European idea, which is based on shared responsibilities”“, this sounds nice, but responsibility also implies accountability, a side that has been absent from the EU and the ECB with ongoing lack of transparency for the longest time, in that Brexit remains a valid step.

So why do I seem to be freaking out?

That is partially true. Not because of Marine Le Pen not making it, which might have solved a few things. It is the part I mentioned yesterday with the Financial Choice Act. As a cheat sheet (at http://media.mofo.com/files/uploads/Images/SummaryDoddFrankAct.pdf)

shows us: “The Dodd-Frank Act creates the Financial Stability Oversight Council (“Council”) to oversee financial institutions“, that part is now effectively gutted from the Dodd-Frank Act. The damage goes a lot further, yet as I see it, the people in the White House have just enabled the situation that what happened in 2004 and 2008 can now happen again. When that happens the Euro will take a massive hit too. With Brexit part of that damage can be averted and in layman non diplomatic terms, we can state that as JP Morgan is getting the hell out of Brexit, the damage they could potentially cause in the near future will be on the books for the places that they go to or remain in.

One of the dangers is seen in the key principles of the Financial Choice Act. With ‘2. Every American, regardless of their circumstances, must have the opportunity to achieve financial independence;‘ we can read it in a few ways, one of them being that this is the sales pitch where the Greater Fool can invest in something, using funds that person does not have whilst endangering whatever financial future they thought they might have had. It basically opens a door to get some of the suckers’ bled dry fast. In addition with ‘3. Consumers must be vigorously protected from fraud and deception as well as the loss of economic liberty;‘, I do not see protection, I see a setting where basic protection is in place, yet as we have seen with the issue in 2008, the amount of people who lost it all whilst prosecution failed to protect the people and convict the ‘transgressors’ nearly 100% is just too stunning, and it is a lot more dangerous now as the global population has nowhere near any level of reserve of protection compared to the last time around. In addition, when larger firms start playing this game, they will drag whomever they passively claimed to protect (like retirement plans, like mortgages they held) with them.

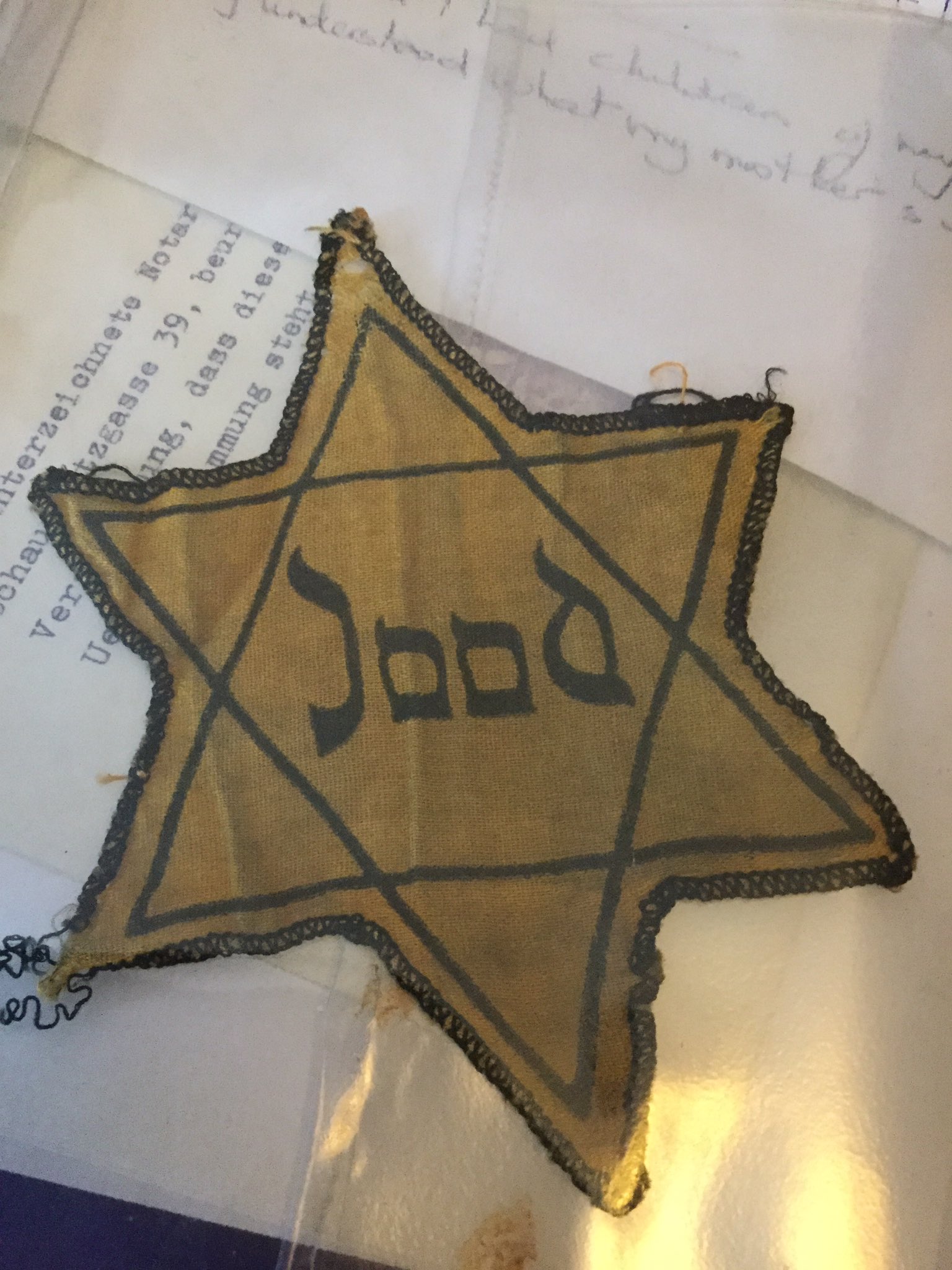

There is another side which takes a little longer to explain. Yesterday someone tweeted an image I remembered when I grew up. You see it is all linked to what I was part of in the 80’s. I saw the application of segregation, isolation and assassination in a less nice way. It drew me back to my childhood, when I was introduced to practices by the Nazi’s in WW2 during my primary school history lessons. To identify the Jewish people, they were told to wear the Yellow Star of David. When I saw the image my thoughts started to align, unlike the puzzlement of the population at large in 1941-1943 as the star was made mandatory in several nations, the people were uncertain to the matter, with the exception of the Dutch underground who would not trust any German for even a millimetre, they were able to hide 25% of the Jews, so in the end well over 100,000 Jews were deported. From those only a little over 5,000 survived. The Dutch underground was able to keep close to 30,000 hidden, with well over 2/3rd surviving the war. Most people, would not learn of the actual fate of the deported Jews until much later, many remained in disbelief for many years after the end of WW2 in 1945. You see, it is that phase that I feel we are in now, we seem to be in disbelief as laws are past to give a sector of industry more leeway, whilst they (according to some sources) made 157 billion in profit and that is in the US for 2016. So you want to open the tap for a system that is less regulated, non-trustworthy and have shown in 2008 to embrace all greed at the expense of anyone else? How is that a good idea?

There is another side which takes a little longer to explain. Yesterday someone tweeted an image I remembered when I grew up. You see it is all linked to what I was part of in the 80’s. I saw the application of segregation, isolation and assassination in a less nice way. It drew me back to my childhood, when I was introduced to practices by the Nazi’s in WW2 during my primary school history lessons. To identify the Jewish people, they were told to wear the Yellow Star of David. When I saw the image my thoughts started to align, unlike the puzzlement of the population at large in 1941-1943 as the star was made mandatory in several nations, the people were uncertain to the matter, with the exception of the Dutch underground who would not trust any German for even a millimetre, they were able to hide 25% of the Jews, so in the end well over 100,000 Jews were deported. From those only a little over 5,000 survived. The Dutch underground was able to keep close to 30,000 hidden, with well over 2/3rd surviving the war. Most people, would not learn of the actual fate of the deported Jews until much later, many remained in disbelief for many years after the end of WW2 in 1945. You see, it is that phase that I feel we are in now, we seem to be in disbelief as laws are past to give a sector of industry more leeway, whilst they (according to some sources) made 157 billion in profit and that is in the US for 2016. So you want to open the tap for a system that is less regulated, non-trustworthy and have shown in 2008 to embrace all greed at the expense of anyone else? How is that a good idea?

So what evidence is there?

Well, there is Senator Warren (Democrat for Massachusetts) who called it an ‘insult to families’, in addition we see “so that lobbyists can do the bidding of Wall Street“, which is still a political statement. When we see the partial part (at http://financialservices.house.gov/uploadedfiles/financial_choice_act-_executive_summary.pdf), we see “Provide an “off-ramp” from the post-Dodd-Frank supervisory regime and Basel III capital and liquidity standards for banking organizations that choose to maintain high levels of capital. Any banking organization that makes a qualifying capital election but fails to maintain the specified non-risk weighted leverage ratio will lose its regulatory relief” It is the very first bullet point and leaves me with the situation that banks have no right to relief when they take a certain path, yet they still get to gamble. I especially like the part in section 4. “Make all financial regulatory agencies subject to the REINS Act, bi-partisan commissions, and place them on the appropriations process so that Congress can exercise proper oversight.” Yet, the REINS Act only passed the Senate, yet is not law at present, in this it is called on to do what? If the Financial Choice Act is set into law before the REINS Act, the US will have a gap the size of the flipping Grand Canyon, in addition, from the McIver Institute we see the opposition from the Democrats with “The REINS bill is similar to legislation moving through congress, but with lower thresholds“, yes, that has proven to be a good idea in the past! Still it is a view of Democrats versus Republicans and it is a Republican government (House, Senate & White House), so wherever are the clear academic dangers? We get that from Mike Rothman, president of the North American Securities Administrators Association and Minnesota commissioner of commerce with “It is clearly evident that the changes contemplated by the bill would significantly undermine and compromise the ability of regulators to effectively enforce financial laws and regulations“, whilst the I saw the term “this voluntary state-federal collaborative framework“, so the collaboration is voluntary, not mandatory. In the last decade, when have we seen a proper level of protection in a voluntary state of any matter?

The beginning of the dangers are shown by the Consumerist, which took a look at version 2.0 of what many regard to be a travesty. In this we see:

- Require the Consumer Financial Protection Bureau to get congressional approval before taking enforcement action against financial institutions

- Restrict the Bureau’s ability to write rules regulating financial companies

- Revoke the agency’s authority to restrict arbitration

- Revoke the CFPB’s authority to conduct education campaigns

- Prevent the Bureau from making public the complaints it collects from consumers in its Consumer Complaint Database

The one I had a stronger issue with is the one that tosses responsible spending around. The issue ‘Remove requirements under the Durbin Amendment that guided how much credit card networks could charge retailers for processing debit card transactions‘, so basically by charging stronger on debit cards, people will see a need to pay cash or force the credit card risk on people who for several reasons prefer not to do so. In addition the restrictions to arbitration will give leeway to Financial Institutions to avoid all kinds of courts as the victims (called consumers and investors in this case) any right to hold the financial institutions to account. It is rigging even stronger an unbalanced system. Marc Jarsulic, Vice President for Economic Policy at the Center for American Progress called this ‘a system that removes protections against taxpayer-funded bailouts, erodes consumer protections, and undercuts necessary tools to hold Wall Street accountable‘, which was already an issue at present making it a lot worse. It seems that the junior workers of 2008 are now in a place where they would prefer to fill their pockets before their luck runs out. The last bit is purely speculative from my side and it might take until 2020 until I am proven correct, yet at present 2 years is a long time to await the dangers of a greed driven system to get a little greedier. It is in that that segregation from the Euro will become essential soon enough, especially as there is no one muzzling the ECB and its crazy need to spend funds that they do not have and will not have for years to come. As for the news we see appear at present on Bloomberg shows my correctness from another side. At https://www.bloomberg.com/politics/articles/2017-05-07/a-reverse-trump-tax-plan-delivers-an-economic-miracle-in-sweden, we see how a reverse of the Trump ideal works a miracle in Sweden. Now, it sounds a little too good to be true and it is. You see, I am not against the principle that Sweden has, yet in Scandinavian terms, the Swedes are uncanny social. I once joked that a woman can get married, after a year she gets the bun in the oven and gets paid maternity leave. If she starts making buns non-stop, she will never work another day (as long as she gets pregnant immediately after giving birth), 20 years and 22 kids later, she still has an income, a sound and secure retirement fund with only one year of work. It is almost true and I admit far far fetched. Yet the social side of Sweden allows for this. Because that one person will be the utter outlier in any statistical graph. The Swedish solution works in a social educated country like Sweden. In America which fosters self-centeredness and greed, this system would be abused at the drop of any hat and the system would collapse. You see, Bloomberg does not mention, that unlike America, companies in Sweden do not shun taxation (IKEA seemingly being the exemption to that rule), which is also a huge difference. In addition, Swedish Civil Law has a sizeable extensive system of Administrative Law which would also contribute. As we see commerce in Sweden increase, the Swedes will automatically feel the brunt of that in a positive way (as I personally see it). Yet it is not all good and summer there, as Magdalena Andersson faces a vote of no confidence if certain changes are not stopped, or even more adamant, be rolled back to some degree.

It is this combined view that France is now seen as ‘Vive La what?’ It is very much on how certain banks and the ECB are called back to stop endangering the future of too many people, Quantative Easing be damned. It is in that environment that the Financial Choice Act is an upcoming danger as Wall Street gets to be in charge of how money flows, in what direction, risky or not. As for what happens between now and 202, I truly hope that I am wrong on every count, because the 2008 global losses which have been estimated to set around $15 Trillion could easily be doubled this time around. More important, as global national reserves are none existent, the impact will hit the consumers and retirees in ways that they cannot even fathom, it makes the hardship in Greece look like a cakewalk as I see it. I will happily be wrong, yet the visibility we already see at present sets me more likely than not correct, which is really scary, not just for me.

Oh and if you doubt me in this (which will remain forever valid), why have we seen massive levels of misinformation from papers with ‘NO ONE wants to risk GREXIT’ Economist says Greece bailout will go ahead to SAVE Eurozone’ (source: The Express), whilst we know that you cannot be set out of the Euro or Eurozone involuntary, and ‘saving Eurozone’ is a little strong is it not? Or the Daily Mail that gives us that Brexit is a gift to the Greeks. This is not merely a point of view, certain sources are adamant to misdirect the focus of the people, if the Euro was such a gift from the gods, misdirection would not have been needed, would it?