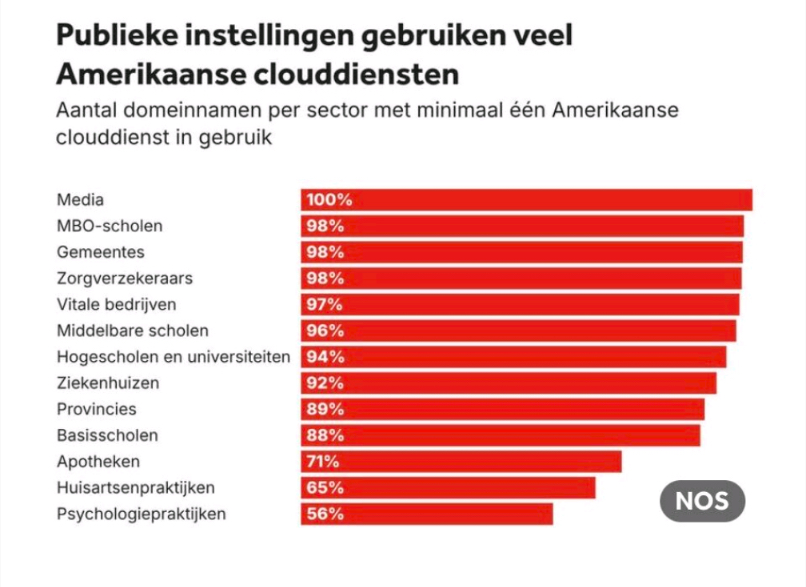

Yup, we are all in that setting, but are we merely waving to the music of Debbie Harry or are we watching the waves from the shorelines. That is merely two options, but when some say that the tide is high, they might be referring to bubbles, the AI bubble to be more precise. I am not some economist saying that bubbles are blasphemy and I am no economist, but I have looked at numbers for decades and the numbers we are given do not add up, and when I was watching Inside Job something hit me, there was a familiar pattern evolving, not evolving, repeating is a better word and I have been saying this for some time. Yet today, a mere 10 minutes ago I see ‘UK Places Microsoft, Google, Amazon And Oracle Under Financial Oversight’ (at https://www.businesstoday.com.my/2026/07/10/uk-places-microsoft-google-amazon-and-oracle-under-financial-oversight/) where we see “The UK has placed Microsoft, Google, Amazon and Oracle under direct regulatory oversight after designating the cloud service providers as critical third parties to the country’s financial system. Reuters reported that effective July 13, the designation covers Microsoft Ireland Operations Ltd, Google Cloud EMEA Ltd, Amazon Web Services EMEA SARL and Oracle Corporation UK Ltd, reflecting the financial sector’s growing dependence on cloud infrastructure”, so whilst the story ends with “The designation will bring the four technology firms under direct regulatory oversight as part of efforts to safeguard the stability and continuity of the UK’s financial sector.” And it comes after we were given (at https://m.au.investing.com/news/stock-market-news/oracle-stock-shrugs-off-sp-downgrade-to-bbb-but-120b-debt-shadow-looms-4526441) where we see ‘Oracle stock shrugs off S&P downgrade to ’BBB-’, but $160B debt shadow looms’ where we see “Oracle Corp. (NYSE:ORCL) shares managed to gain 2.7% on Thursday, defying a credit rating downgrade from S&P Global Ratings. While shares edged slightly lower from their midday highs, the tech giant still traded firmly in positive territory. Investors chose to focus on Oracle’s staggering $638 billion backlog of cloud contracts rather than the immediately apparent threat to its balance sheet: S&P downgraded Oracle’s long-term issuer credit rating to ’BBB-’ from ’BBB’, retaining a stable outlook.”

Now, I am not having anything against Oracle. They have always been on the foreground of technology and innovation in its field and it is unlikely to ever change. But there is a larger setting, the entire AI bubble as I see it, it will hit them too. They all over invested in that setting and they are likely the biggest catchers of the implosion of that event. But I am still in arms over ““The official position of the Secretary and the U.S. Treasury is that Artificial intelligence will be a key driver of America’s new Golden Age,” the spokesperson said. “AI has the potential to deliver unprecedented productivity gains, expand economic opportunity, and empower American workers and businesses.”” You see, there is no golden age, there is no AI, not yet at least. There is DML and LLM and they are great, they can hand innovation and prosperity in several ways. It merely isn’ AI and that needs to be said, because soon the class actions will go for the “It’s AI and we cannot really predict what AI does” but it isn’t, it is DML and that requires a programmer, it requires data and these two hinder stones are the backdrop for prosecution. Only last week we were given ‘Anthropic Faces a New $75 Million Lawsuit for Pirating Books to Train Claude AI’ and less than 24 hours ago Harvard Business Review ‘You Outsourced the AI—but you still own the risk’ where we see “As enterprises increasingly embed third-party systems into their workflows, technological risk has led to new legal and operational responsibilities. Leaders may have little visibility into how a model was trained or how it changes, yet when it discriminates, mishandles data, or harms a customer, regulators and plaintiffs often look first to the company that deployed it. Peloton learned how that exposure can arise. Visitors to its website see a familiar invitation to “chat,” powered by a third-party vendor. According to a class-action complaint, the vendor recorded and stored conversations and used the data to improve its machine-learning models. Peloton neither built nor trained the system. Even so, a California federal judge allowed a claim against the company to proceed. The parties later jointly dismissed the case, without publicly disclosing the terms.”

Now consider the amalgamation of these factors (apart from some saying there is no bubble) there is (allegedly) “Worldwide spending on AI is forecast to reach $2.5 trillion. Venture capital and private corporate investments in AI firms sit near $258.7 billion globally, with over $750 billion in dedicated infrastructure and data center capital expenditure from major tech hyperscalers” we then see that the big players (Microsoft, Google, Amazon, Oracle) are basically overextended, facing class actions and all of them are looking at all sorts of financial hardship, because at some stage all these players will be made to rephrase the simple truth that AI is not DML/LLM, it requires more and when the programming is put under a loop that setting comes crashing down. I saw it two years ago that this is the only outcome in some sales people overselling what they had and the simplest setting is not a mere Quantum computer. It requires shallow circuits and what I tend to call The Epsilon processor. True AI cannot exist in a binary setting. The last one is my interpretation of it all and some might disagree. But the Epsilon processor allows for Null, False, True, Both and it is the Both part that makes true AI possible and of course a matching operating systems will be required as well a data carrier and in that case Oracle and Snowflake have the grounds for success. As I see it, all others will fall behind these two.

And last month we were given that “400 newspapers sued OpenAI and Microsoft for scraping their content without permission or compensation to train artificial intelligence programs” even my data has been scraped. So how many will be successful? How many will fail? I have no idea, but the odds are decently stacked against these salespeople. And as the courts rule against these Fake AI bringers (as I see it) there will be a rush of people making a case, all who were sold AI (without clear DML/LLM settings in their contracts) are seeing their pupils transform into dollar signs and they will try to clean house. So when all these settings happen, is the stage for a bubble that far fetched?

I am watching and watching and noting what is due. I reckon that at some point I get the one piece of evidence that will allow me to do just that, 2700 (out of nearly 4000) article scraped seemingly give me an optional case for some dollars (five million plus would be great). And I am not the greediest player in town. So at what point will the investors of $2.5 trillion ring the bell wanting to see payment for their investments? Goldman Sachs gave us last month ‘The AI Investment Boom: When Will It Pay Off?’ With “The economics of artificial intelligence are more questionable today than two years ago, says Goldman Sachs Research’s Jim Covello, as enterprise buyers, model companies, and hyperscalers have yet to show returns on their spend. In a conversation with Alison Nathan and George Lee on Goldman Sachs Exchanges, Covello discusses where we’ve seen economic value accrue to date and why semiconductor companies can’t continue to be the sole beneficiaries of the AI buildout.” As such we see people with serious economic skills worrying and wondering what comes next and I was there at least a year ago. So when will others see the doubt that I am seeing? The money people call the bubble a blasphemy, but they have vested interests. I do not. I merely see the flaws on technology that is at least 15-20 years away, data that is largely unvalidated and unverified and at this juncture people are investing trillions? Makes me all tingly that too many people are greed driven and too much vested to be part of a boom that does not exist, just like the settings of 2008, Inside Job showed that clearly and it seems that we have a similar setting evolve at least two times the previous caper. So if you consider that with all the reserves that hit took the economy 2 decades to fix and at present the reserves are gone, so what will happen now? Why aren’t others taking the stand the UK is making? Because others are in the believe that “America’s new Golden Age” is here? When you realize that it will take close to two decades to arrive, how long until too many investors pull the plug and go somewhere else? What will happen then? That is what I see coming, because at some point more and more people wake up, this is bound to happen, it always does.

So is the water high enough? Have a great day.